Welcome back, Dear Reader, to the latest quarterly missive from Nick Lincoln. This edition has FIVE articles.

If for some bizarre reason you enjoy “The Hat-Tip Newsletter” please do forward it to family and friends.

THE AUTUMN STATEMENT: A DECLARATION OF WAR

HUNKER DOWN AND PUT UP THE FINANCIAL BARRICADES: YOUR WEALTH IS NOW VIEWED AS COMMON PROPERTY

At least now it is in the open, no longer up for debate. The battle lines have been drawn. The UK now officially consists of those producing, and a parasitic class taking from the productive. This Month's Chancellor has not tried to hide the intentions of this latter group: the parasites see your money as rightfully theirs. His Autumn Statement further increased the already enormous tax burden on those working, earning, and providing.

And for those of you living off your hard-earned savings and enjoying your leisure years? Fear not: Chancellor Hunt is after you as well.

I think this is evil. I will go down swinging to protect as much of my wealth as I can from the parasite’s looting grasp. And I will try and do likewise for you if you will let me.

How It Began

First a brief history of where we were, so as to better understand where we are. Taxes of various sorts were introduced in the UK as far back as 1203 with an export tax on wool. Following the Great Fire of London in 1666, Charles II introduced a tax to help rebuild the City. From our history lessons, many of us will remember the 1707 Window Tax.

But the above were trifling measures. Things didn't get serious until the budget of December 1798, when Pitt The Younger introduced Income Tax to our lives, notionally to pay for the impending Napoleonic Wars. Once the door was ajar, the looters went nuclear: in 1803 Prime Minister Henry Addington introduced schedules into our taxation system (they’re still with us), and legalised theft was off and running:

Schedule A (tax on income from UK land)

Schedule B (tax on the commercial occupation of land)

Schedule C (tax on income from public securities)

Schedule D (tax on trading income, income from professions and vocations, interest, overseas income and casual income)

Schedule E (tax on employment income).

Throw in a couple of World Wars, a rapacious and never-sated Welfare State and public sector, and you have a tax code that is enormous, barely comprehensible to all but tax specialists, and a creeping fear that the looters will never have enough until they have everything that was once yours.

“We contend that for a nation to try to tax itself into prosperity is like a man standing in a bucket and trying to lift himself up by the handle.”

Where We Were in 2010 Under Labour

In the 2009-10 financial year, with a Labour administration that had been in power since 1997, the top rate of Income Tax was 40%, levied on all taxable income over £37,400. Dividends had their own rates but were effectively treated as tax paid unless you went into the higher rate tax bracket. Corporation Tax was 28%.

There was no 45% Additional Higher Rate of income tax. There was no tapering of the personal allowance for those on incomes over £100,000.

The amount you could legally shove into your pension fund each year (the Annual Allowance) was a staggering £245,000. And the Lifetime Allowance - effectively how much you can accrue in your pension over your, er, lifetime - was a juicy £1,750,000. The Capital Gains Tax (CGT) allowance was £10,100 a year.

Remember that the above was the tax landscape after the Great Financial Crisis of 2007-9, the then "Catastrophe-of-Catastrophes"© du jour, when politicians of all hues clamoured for more of your money to help the banking system they had decided to bail out.

To ram it home: this was the relatively benign tax landscape in Britain after 12 years of socialism.

File under “No shit, Sherlock”.

Where We Are Now

Prior to Chancellor Hunt’s Autumn Statement/Budget, after 12 years of a supposedly “Conservative” government, the UK tax burden was at its highest since the end of World War Two. Despite this, we were mired in record debt. So Hunt’s solution to the ever-increasing debt? More taxes.

From April 2026 income tax at 45% will now be levied on income over £125,000, previously £150,000. The tapering of the personal allowance remains, which results in a marginal rate of 60% (!) on earnings between £100,000 and £125,000.

All income tax thresholds have been frozen until 2028. The personal allowance remains at £12,570, unchanged since 2019. As in previous years, someone earning over £50,700 will pay the higher rate tax of 40%.

Freezing allowances are a clever way to skin the cat. This is “fiscal drag”. Sadly not a description of Eddie Izzard as Chancellor (some image), fiscal drag is a stealth measure that sees people paying progressively more tax as their incomes and wealth (particularly property) grow.

As noted above, the current personal allowance was set in 2019 and is to remain at that level until 2028. As an example, if inflation averages 4% over that period, the personal allowance would need to be £17,891in 2028, just to keep pace with rising prices. Instead, it will be £12,570, meaning more and more people pay Income Tax.

It used to be quite a thing to be a higher-rate taxpayer. Nowadays train drivers fall into that bracket (not that there’s anything wrong with being a train driver. When they’re working and not striking I’m sure they’re worth every penny).

Other examples of fiscal drag?

The Inheritance Tax (IHT) allowance remains £650,000 for a couple. It’s been at that level since 2009 and will remain so until 2028.

The pension annual allowance remains at £40,000. The lifetime allowance will remain at £1,073,100 until April 2026. The ISA allowance has been £20,000 since 2018 and will stay there until 2026.

And if fiscal drag isn’t aggressive enough for you, Chancellor Hunt has kindly thrown in some other beauties.

Corporation Tax is due to rise by a third next April, to 25%. Once this has been paid, from whatever is left over, company owners (formerly known as “wealth-creating entrepreneurs” but now commonly referred to as “flat-out mugs”) can pay themselves dividends to be taxed at increased rates AND with a lower annual dividend allowance (once £5,000 it will be just £500 in a couple of years).

This move alone will also see thousands of retirees with investment portfolios having to complete tax returns to declare meagre dividend incomes. Bet you didn’t vote for that last time at the ballot box.

The annual Capital Gains Tax (CGT) allowance is to fall by a staggering 75% by 2024, from £12,300 to just £3,000. Amongst other things, this tax is levied on profits made when buying and selling buy-to-let properties. Many investors in this sector must be wondering why they ever bothered.

Those windfall shares that you’ve held on to for years thanks to inertia? Could well be that you will now have to pay CGT on them when and if you eventually sell them. Again - you will have to complete a tax return as a result.

You can avoid CGT by dying but for most people, this is a somewhat extreme solution as it puts on a severe crimp on social engagements.

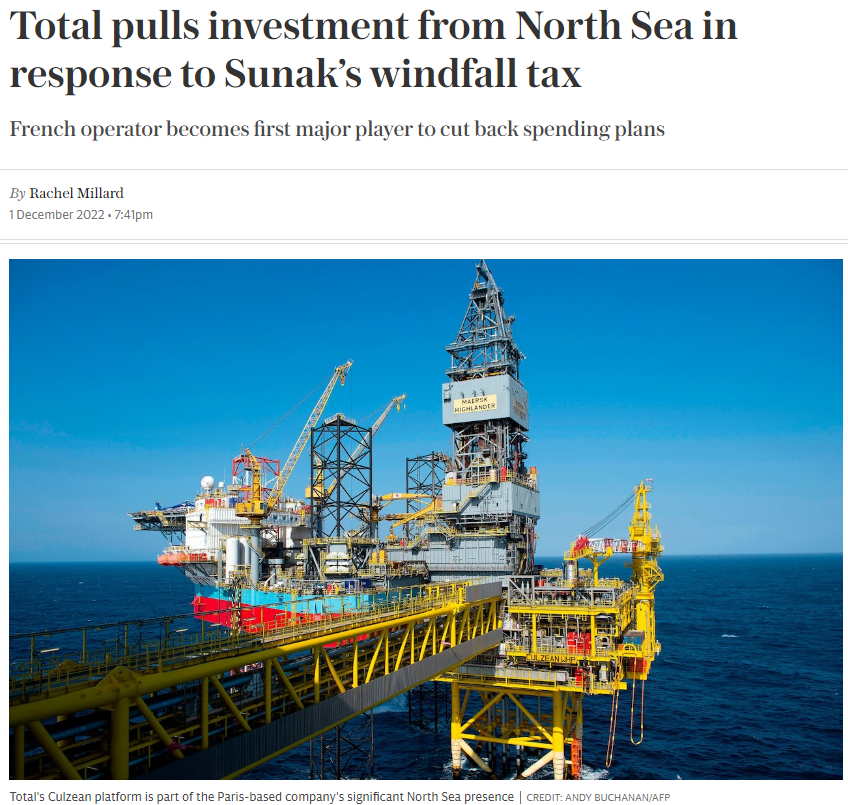

Time for one final loot? The “Windfall” tax on energy companies will rise from 25% to 35%. No doubt the Government will quickly cut this tax as and when energy prices stabilise or fall. After all, a tax brought in because of extraordinary circumstances must surely go when those circumstances vanish. Let’s see. Already oil companies are responding exactly as anyone with a brain could have foreseen (see the above image).

This is a Conservative government doing all this. Just in case you needed to be reminded.

Planning Going Forward

The message is clear. The Conservatives want your money as much as a Labour administration would do. They have declared war on the wealth creators, those in work, and those looking to leave legacies for loved ones.

Now, more than ever, it is essential that we keep making sure our remaining allowances are fully used, year-on-year. Plain vanilla strategies that have always worked remain front and central to all of our financial plans. These include

using your ISA allowance each and every year. A couple can shield £40,000 from HMRC and not worry about dividend or capital gains taxes (and the resulting tax returns);

ploughing as much as you can into low-cost, transparent pension arrangements, allowing you to claw bit a tiny bit of the taxes you pay;

using your annual CGT exemption to “wash through” investment profits tax-free. This is going to get much harder going forward, however!

arranging your affairs so as to leave as much as possible to your heirs, not HMRC.

Don’t be sucked into high-risk, convoluted tax-avoidance schemes. These are often expensive, highly dubious in character, and open to later appeal and reversal by HMRC and the courts.

As and where the Autumn Statement brings in changes that affect individual clients of Values to Vision, we are in the process of contacting you to advise on appropriate planning tactics and/or will advise you at your Annual Planning Meeting.

Make sure you pay all taxes you legally have to. But before doing that, use all legal means to reduce your tax bill. You owe it to your future self and those you will leave behind.

“The hardest thing in the world to understand is income taxes.”

PUTIN’S PUNY PRICE PUSH

HIGH INFLATION (THE “COST OF LOCKDOWN” CRISIS) WAS ALREADY IN THE SYSTEM BEFORE VLAD’S EFFORTS MADE THINGS WORSE.

No one likes a smart arse, which might explain my ever-dwindling list of party invites. Nevertheless, for this piece, I’m donning my full “Told You So” regalia. Back in the Autumn 2021 Hat-Tip Newsletter, I wrote about the re-emergence of inflation.

I’m no expert in chronology but that strikes me as being a good five months prior to Putin’s Ukrainian assault toward the end of February this year.

Blaming the current spike in prices solely on Putin is a flat-out lie, a classic “deflection” tactic. Putin’s actions in Ukraine have indeed placed enormous strains on energy supplies, and food prices may continue to soar as that country’s importance to grain production becomes ever more clear.

We cannot do much about the latter but the energy problem is entirely of our making: for years we’ve outsourced our decision-making in this area to a perpetually petulant Swedish schoolgirl and her brigade of Eco Loons, all of whom will be salivating over the very likely prospect of National Grid shutdowns this winter.

Simultaneously somebody, somewhere, seriously thought it was a good idea to make us energy dependent on despots, in Russia and elsewhere (looking at you, Saudi Arabia and ilk).

Some truth in this. But the money printing presses were running at full-pelt before Ukraine.

But the Ukraine issue has merely accelerated inflationary pressures that were already gathering momentum. If Putin didn’t exist, we would still be facing a torrent of rising prices and concomitant rising wage demands. These are a direct result of the West’s reaction to The Wuhan Flu of 2020-21. In essence, Governments:

Deliberately and for the first time in history, put their economies into a coma. Businesses were told to stop producing. Employees were sent home to sit on their backsides whilst bribe - “furlough” - money came into their bank accounts. Of course, production (GDP) fell off a cliff - a fall in economic output not seen since The Great Frost of 1709.

Ramped the printing presses up to full speed, spewing out money to fund these bribes, the loans to businesses, and relentless full-page propaganda press advertising (about the only thing stopping the Dying Legacy Media from going to the wall). And of course, all those masks and completely empty emergency hospitals didn't pay for themselves.

“Inflation is always and everywhere a monetary phenomenon, in the sense that it is and can be produced only by a more rapid increase in the quantity of money than in output.”

So what happens when you combine a dramatic, unprecedented decline in output (GDP) with a massive increase in the quantity of money circulating? What would history tell you happens when demand greatly exceeds supply?

Inflation. Steeply rising prices. When too much money chases too few goods and services it always leads to inflation.

So that’s where we are now. Many of us are looking at the unholy trifecta of declining real incomes (thanks to fiscal drag); rising mortgage costs; and a sharply increasing cost of living.

Hunker down, control what you can control, cut out the inessentials, and wait for the better times to return.

And return they will - they always do. It’s just hard to say when. In the meantime, continue saving and investing for your future self. One day you will be grateful you had the fortitude (and advice) to keep on keeping on.

But for now, don’t accept the spin. Putin hasn’t got us in this mess. WE HAVE, or rather those we elect to serve us have. Never forget.

putin or not, the great companies of the world continue to offer sanctuary from inflation. seek that sanctuary and “this too shall pass”.

“The root of joy is gratefulness. It is not joy that makes us grateful; it is gratitude that makes us joyful.”

WINTER PRACTICE UPDATE

DESPITE FIDDLING WITH THE THERMOSTAT, THE HEATING IS BACK ON

Nick Lincoln, IFA and owner of V2VFP Ltd

Already the glorious summer seems like a hazy fable. Like many of us, I’ve nudged the thermostat down a degree or two in fear of impending energy bills (thanks Greta and Vlad).

Annoyingly, the heating is coming on regardless, as we move rapidly into that season still known as Winter, despite Global Warming.

Those of you who closely read these missives (I love you both) will have noted that last time around, I mentioned that The Lovely Penelope (TLP) and I got married in the Summer. As I type, I am happy to report this remains the case. I know some of you need continual reassurance that this amazing lady and I are still together - I believe it’s called “the suspension of disbelief”.

And the good news keeps on coming.

In the last few months, my practice has taken onboard new clientele. Welcome to Jeremy, Neil, Sam, Caroline, and SL. As ever, all of these were referred to me by existing clients, to whom I remain indebted. Helping people to put in place sensible, bespoke financial plans that underpin their life goals remains something I absolutely love doing. Yet, I am of an age where it’s not uncommon for me to be asked when I plan to retire. My answer? Probably never, as long as I have my faculties (stop sniggering at the back).

For reasons that escape me, I am seemingly well-regarded by a small cohort of like-minded financial planners, and from this, I derive a certain level of esteem. Is that needy or insecure? I don’t know. But I do know I would miss this aspect of my career as and when I called it a day.

By way of example, I spoke in November at Humans Under Management (HUM), the premier UK event for financial planners (and it’s not even close). I speak at HUM every year, which remains a mystery: it’s not unusual for me to be asked to speak at events but it’s very unusual for me to be asked back.

Nick commands the stage. Or something.

Nothing quite sharpens the mind like speaking in front of at least 200 of your fee-paying peers (with another good number watching virtually from their homes/offices). The speech was seemingly well received. By which I mean I escaped alive and was only admonished for causing offence by a couple of attendees, which - to me - is a win.

Practicing Gratitude

We enter a season of family, reflection on the passing year and anticipation of a new one. As ever, now is the perfect time to remember how fortunate we are, despite our travails.

To my clients: I thank all of you for your continuing faith in my services. To the casual reader: thank you for your time.

TLP and I wish you a very Happy Christmas and let’s hope that 2023 is everything we all wish it to be - and more.

Until the Spring then, Dear Reader. Take care.

“You know what a friend is? Someone who knows all about you and likes you anyway.”

FTX: "WORSE THAN ENRON"

WE DON’T GO NEAR CRYPTO. WE LEAVE THAT TO THE “PROs”

This is not the time or place to talk about crypto in the round. I’ve avoided doing so for this long and I’m not going to start now. Life’s too short to waste on such frippery.

However, sometimes you can’t avoid being drawn into a deep well of schadenfreude. And the collapse of FTX is an absolute masterclass in greed, ignorance, vanity and hubris.

Where to start? Let’s focus initially on Sam Bankman-Fried, or Scam Bankrupt-Fraud (SBF either way), former FTX Chief Executive: an entitled, overweight juvenile. Wearing trainers and Primark-special romper-suit stuff to high-level pitch meetings? How brave. How stunning.

“A man is known by the company he keeps”

How about the rats swimming in the same sewer? What a rogue’s gallery on stage with him, desperate to once again be relevant, and get some reflected glory just by being seen with Mr Chubby, who obviously can’t let go of his phone in case his brain explodes.

Turns out SBF was the second single biggest donor to The Democratic Party in the USA, behind only the ever-lovable George Soros. Funny how the FTX collapse happened literally just days after the recent mind-bogglingly expensive mid-term elections.

But never mind the Clintons and Blairs of this world. What about the real pros such as the hedge funds? These are the guys and gals who really know how to evaluate the price of everything. They can spot a scam from a million miles.

Or not.

In further proof that there may indeed be a God, “hedge funds have billions of dollars stuck on failed cryptocurrency exchange FTX”. There could be up to 150 such funds. Turns out the pros - hardwired to avoid FOMO (Fear Of Missing Out) - looked beyond the numerous red flags that lay around SBF and his company, and decided proper due diligence was for the squares.

“Be Aware: Stay Square”

Without a doubt, this is fraud on a monumental scale. Indeed, John Ray III, the man brought in as CEO to oversee the FTX bankruptcy process, said he had never seen “such a complete failure of corporate controls”. And he should know. This was the man brought in to do the same thing as Enron collapsed in late 2001.

For context, at the time, Enron was the largest bankruptcy reorganisation in U.S. history. And John Ray III thinks FTX is worse.

Meanwhile, you and I, Dear Reader, do what “the squares” have always done. We don’t chase fads. We don’t invest in things we don’t understand. We don’t seek status or kudos from our portfolios. We don’t search for outlandish and unnecessary investment returns, because we know such returns can only ever come attached to a commensurate level of risk (defined in this instance as permanent loss of capital).

Past performance is no guarantee of future returns. The figure quoted is net of fund management fees but does not include custodial (platform) or advice fees.

No, we “squares” simply invest in The Great Companies Of The World (TGCOTW) and then, figuratively, pivot our chairs to the left or the right (the latter, ideally) and stare out of the window for the next three decades and more.

Over the last decade (it’s only been going since October 2008), our super-simple, four-funds-only 100% GCOTW portfolio has returned an annualised 11.1%. Have other investors done better? Probably. Have many more done worse? Certainly.

Unlike Aesop’s arrogant and hubristic leporid, we passive leatherbacks just keep on grazing and digesting the long-term market return. In so doing it turns out we accrete real wealth and see our financial plans reach attainment, with the least amount of hassle, costs, and taxes.

aS THE TORTOISE YET AGAIN BEATS THE HARE, PERHAPS ALL INVESTMENTS SHOULD COME WITH A HEALTH WARNING: “BE AWARE - STAY SQUARE”

INFLATION IS TO RETIREMENT WHAT CARBON MONOXIDE IS TO HEALTH

This is a recurring piece. Each quarter the figures will be appropriately updated. Why? because while the numbers will change around the edges, the message is eternal!

A typical retired couple may well see one partner live for three decades or more. Over such a long period, the annual cost of Lifestyle could more than triple. Says who? Says me: financial planning involves enormous ambiguity. If you want certainty, die now.

So an example Lifestyle cost of £50,000 per annum entering retirement could later escalate to £150,000 a year, just to keep standing still, to keep buying the exact same amount of “stuff”.

If you really must, some prosaic evidence: in 1992 a First Class stamp cost 24p. Now? 95p. See the detailed graph below:

Some nuggets to lessen the gloom (past performance is no guarantee of future returns etc):

Three decades ago - Winter 1992 - the S&P 500 (The Great Companies of The USA) was valued at 435;

Today, 30 years on - Winter 2022 - The Great Companies of The USA are valued at c.3,960;

In three decades these Great Companies have grown in value by a factor of nine;

In addition, the dividends paid by these Great Companies have risen five-fold in those 30 years.

The last three decades have seen four "get me out of here I can't stand it anymore" bear markets (2001-3, 2007-9, Q1 2020 and right now) and numerous smaller temporary declines.

Source for US market figures here. Why US data and not the UK? Because the Yanks have this kind of thing publicly available and we don't - yet. Also, the US market is enormous. By comparison, the UK market - at under 5% of worldwide market capitalisation - is tiny.

Dear Reader, the big risk to a dignified, independent retirement Lifestyle is the destruction of purchasing power via inflation. Like carbon monoxide, you can't hear it, smell it, see it, taste it. Yet inflation will silently, stealthily kill your wealth.

The cure? Possessing a Financial Plan fueled by ownership of The Great Companies of The World: equities.

The problem with the cure? It's really really hard to stick with your Plan and stay invested through the horrendous-but-always-temporary-declines. The cure for the cure? Having a tough-loving, empathetic counsellor to stand between you and "the big mistake".

Having stated the problem, and maybe scared you witless, I hope the above figures give you a glimpse as to the only rational, moral solution for a healthy couple facing a three-decade plus retirement!

“Inflation: odourless, tasteless, and utterly poisonous to a dignified, independent retirement.”