Welcome back, Dear Reader, to the latest quarterly missive from Nick Lincoln. This edition has FIVE articles.

If for some bizarre reason you enjoy “The Hat-Tip Newsletter” please do forward it to family and friends.

THE ETERNAL UNASKED QUESTION

ONCE AGAIN THE DYING LEGACY MEDIA HAS THE TELESCOPE BACK TO FRONT

Clients will know my views on personal finance media. Even the most acute brain can be led astray by some fantastically awful puff piece promising the earth for little more than a grain of sand: where minds meet money is a strange place of roiling emotions and fear: Fear of losing everything in some unprecedented phantasmagorical disaster or - more perniciously - fear of missing out on the next big thing the loudmouth at the golf club/gym/hot yoga/pilates group [insert leisure pursuit of choice] drones on about.

The personal finance media (or the comic section, as it should be known) preys on these hard-wired fears. It really does exist only as clickbait. It serves no educational purpose. Like consuming a family size bag of Wotsits (for those not in the know, this is a maize-based snack with zero nutritional value), personal finance pieces titillate during consumption, only to leave you feeling grubby and slightly soiled afterwards.

I keep abreast of it solely to “know thy enemy”: if I am cognisant of the latest filth out there, perhaps I can prevent someone from acting on it in a way that is almost guaranteed to be injurious to their long-term financial wellbeing.

By way of example let me present this online piece from February. According to its banner, “This Is Money” is the “Financial Website Of The Year”. Heaven help us. What must the competition be like? Anyway, the premise of the piece is that “Grandma” has £100,000 to invest to provide her with an income of around 3-5% per annum.

Apparently, this must be achieved with no loss of capital, as “capital preservation is paramount.” And because this fatuous statement is taken at face value, the piece races off down the usual rabbit hole of dimwit talking heads opining about natural income (fetch my gun), bond yields, attitude to risk, capacity for loss, and a whole load of other dross that, in a just world, would see the perpetrators flogged to within an inch of their lives.

As an aside, all of the recommended “solutions” to Grandma’s dilemma seem to involve expensive, active fund managers, the very people whose funds are so heavily advertised in both the print and online money sections. Just sayin’

To my point (there is one, bear with me). What if Grandma had been asked the eternal unasked question? What if she had been asked, “What EXACTLY do you mean by capital preservation?”

What if Grandma had been asked the eternal unasked question? What if she had been asked, “What EXACTLY do you mean by capital preservation?

Imagine the scene. Silence crashes down as Grandma is given all the time in the world to formulate her response to these eight words.

The silence holds. She will and must crack first.

Eventually, perhaps, she responds as per below, and the conversation flows:

Grandma: “Well, I don’t want to lose any of it.”

Caring, empathetic adviser (CEA): “Of course. Without getting under your skin, what precisely do you mean when you say ‘lose’?”

Grandma: “I mean ‘lose’, moron. What do think I mean?”

CEA: “Forgive me if I’m wrong - I frequently am. I think you mean you can’t afford to have this pot of money fall in value. Because if it falls in value, it will buy you less and less. And if it continues to fall in value, one day it will be worthless. Am I warm?”

Grandma: “Spot on. For a moment there I thought you were an idiot in search of a village. Have another biscuit.”

CEA: “Thanks [reaches for a custard cream]. Now we’re beginning to understand each other, another question, if I may: how would you feel if the value of your investment fell by nearly half over the next 20 years?”

Grandma: “I’d feel I’d wasted a packet of biscuits on you. Is there a point to this? ‘Countdown’ is on in five minutes and I need to prepare.”

CEA: “Understood. I’ll wrap it up. You’re 70 now, although I find that hard to believe. Let’s assume you live another 20 glorious years. I don’t give many guarantees and I certainly never give them when it comes to investing. But what I CAN guarantee is that your £100,000 will almost halve in value in terms of what it can buy you if inflation averages 3% a year over the next two decades.”

Grandma - who remembers a time when inflation was double-digits for decades - loses some of her youthful blush and presses ‘Pause’ on the Sky box remote. “What did you just say, young lady?”

CEA: “I believe in the maxim of telling people what they need to hear, not what they want to hear. I have just told you that seeking capital preservation is about the most dangerous pursuit anyone with any decent amount of time on their side can follow. You have that decent amount of time. Instead of pursuing ‘capital preservation, would you agree that what we need to do is work to preserve the purchasing power of your £100,000 over the next 20 years?”

Grandma: “Yes. This all makes sense. Why don’t they talk about this in the - what did you call it - the comic section?”

“Successful people ask better questions, and as a result, get better answers.”

CEA: “Because telling people the truth about money, about the real risk being inflation wiping out the purchasing power of their money, doesn’t generate the clicks. Those custard creams are starting to back up. Do you have any Hob Nobs?”

The conversation continues, now framed by the spectre of inflation as the real risk to Grandma’s future financial well-being. This naturally leads to ways of mitigating two decades’ worth of rising prices. With a required return on capital of between 3-5% per annum after fees, the discussion cannot help but focus on the inflation-beating wonders of the long-term compounded return of The Great Companies of The World (shares, equities, whatever you want to call them).

Whether Grandma goes down this route is up to her. She is told that every five to seven years she can expect around a 30% temporary decline in the value of a portfolio invested in said companies. Sometimes it can be more than this. She’s told it’s always temporary and that we try to mitigate this risk to her capital by having around two years worth of future income in cash, so we are not selling into a falling market.

In the end, it’s her call. Her Caring Empathetic Adviser has laid out the cards and spoken the truth as she sees it. She knows that since January 1970 the very worst 20-year return that the Great Companies of The World have delivered was 5.1% per annum, from April 2000 to March 2020 (source: MSCI World Index).

"Capital preservation is paramount." Here is the fallacy of the Dying Legacy Media: all that matters to these dopes is that the same amount of currency/money/paper is always there. That in this example inflation can silently halve its real value is apparently of no consequence.

TO GET THE RIGHT ANSWERS, find a financial adviser who will ask you the right questions

INFLATION NATION

AFTER DECADES OF BENIGN INFLATION, THINGS MAY BE ABOUT TO GET ALL WILSON-HEATH-CALLAGHAN

Just to be clear: this piece is not predicting anything. After years of careful research, I still cannot estimate the perfect cooking time for a poached egg; if you think you are going to be wowed here by some forensic insight as to what might happen to prices, the markets, or the economy, you are going to be disappointed.

Nevertheless, it would take plutonium grade ignorance to not have noticed an uptick in UK inflation in recent months. And a quick Googling of “rising inflation” shows that concern about rising prices is a worldwide phenomenon, from the USA to China to wherever it is outside of Broadcasting House that The Guardian is still read.

Over the last two decades and more, UK inflation has been relatively kind, at around 2.8% per annum. Whilst we rightly perceive low inflation as being “better” than high inflation, as another article in this newsletter points out, inflation at just 3% a year will, in two decades, almost half the value of your money in real terms.

This, perhaps, is why the recent increase in the rate of inflation gets the pulse racing somewhat. If benign inflation is ultimately corrosive to your savings, what on earth could malignant price rises do? And what can be done about it?

Let’s put things into some sort of perspective. Most of you Dear Readers will have some hazy recollection of the 1970s and 1980s. Some of you will even remember the 1960s (although if you can, you probably weren’t there, to paraphrase Charles Fleischer). This was a time when UK inflation was regularly double-digit: in the year to August 1975, UK Retail Price Inflation hit 27%!

The 1962-1991 Great Inflation. Figures are annual returns.

Source: Dimensional Fund Advisors (sic)

In what I call “The Great Inflation” - running three decades from January 1962 to December 1991 - the UK went through seismic events as it tried to grapple with a decaying industrial base, militant unions, lacklustre industrial management, and steadily mounting inflation.

This period (including various bumbling Prime Ministers, from Macmillan to Wilson to Heath to Callaghan to Major amongst others) was scared by industrial unrest and economic embarrassment.

In terms of UK inflation over the period 1962 to 1991, the numbers are pretty gruesome. The Retail Price Index averaged 8.1% over that time! So unless your pay was rising by at least that amount each year your real wages were in decline. Cue industrial unrest and thousands of days lost to strikes, which reached peak lunacy in the 1970s (a decade so whacko that Jimmy Saville, Rolf Harris, Stewart Hall et al were some of the biggest stars of children’s TV).

“The collective best guess of investors as aggregated by market prices is hard to beat as a guide to what the future may hold. Investors may therefore be best off tuning out the pundits and figuring out how to either outpace or hedge against the inflation that’s already anticipated in market prices….

Investors don’t need to outguess markets or undermine their portfolio objectives to outpace or hedge against inflation. They should, however, avoid overreacting to short-term fluctuations in consumer prices.”

Inflation clipping along at 8.1% a year for THIRTY years does no one any real good, although “borrow now, repay maybe later” Governments and everyone else in debt loves it, as inflation basically pays off debt with little real effort involved. This might be one of the reasons homeowners of the 1970s and 1980s fell in love with property: property prices rose massively in nominal terms, and inflation helped wipe out the real value of mortgage debt.

For the saver, or someone living off a fixed income, inflation is a disaster. £100 in January 1961 would be worth just £10 in December 1991. 90% loss of purchasing power in 30 years! Wow. Put another way, Mrs Miggins would have needed £1,035 in her purse in late 1991 to buy what £100 would have got her at the start of 1962.

Are we heading back to these kinds of horrific figures? I have no idea. I certainly hope not. But - but - if we are, once again I ask you to consider the essential soothing qualities of owning a beautifully diversified portfolio chock-full of The Great Companies of The World.

Talking heads regularly bleat on about how share prices are impacted by inflation. My take? During the Great Inflation of 1962-1991, the Great Companies of The UK returned FOUR times the real return (eg allowing for inflation) of “safe” Government gilts (a decent proxy for cash savings).

A Quick Word About Gold

Gold is often touted as the bee’s knees when it comes to warding off inflation. The facts, however, don’t support this argument.

We’ve just “celebrated” the 50th anniversary of President Nixon taking the USA off the gold standard, at Bretton Woods, New Hampshire, in August 1971.

For the rest of that decade, people bought the gold that was previously tied up at The Federal Reserve. Its price rose correspondingly. And then it stopped rising. In fact, for the three decades from January 1980 to December 2009, the price of gold fell in real terms by 29%! Source here.

Please don’t talk to me about gold.

Ever.

It looks pretty if that’s the bag you’re into. Aside from that, it’s an inert metal with no intrinsic value: it doesn’t produce anything and it doesn’t yield an income. You buy it and hope someone else one day will buy it from you at a higher price.

last time i checked, “hope” is not an investment strategy.

“Don’t cling to a mistake just because you spent a lot of time making it.”

AUTUMN PRACTICE UPDATE

the URCHINS are back at school, the traffic’s bad (and that’s good), and we’re getting back to the better place

Nick Lincoln, IFA and owner of V2VFP Ltd

How was your summer? Did you manage to get away for a jaunt overseas? Or did you - like my mechanic John - baulk at forking out £800 for the ̶O̶r̶g̶a̶n̶i̶s̶e̶d̶ ̶R̶a̶c̶k̶e̶t̶ testing process so four ordinary people could possibly, just possibly, enjoy a cheap all-inclusive week on Cos?

Perhaps you instead spent some time exploring the delights our country has to offer. This seems to have been the experience of nearly everyone I’ve spoken to.

And why not? What a beautiful country England is. If nothing else, The Great Reaction to That Wuhan Thing has almost forced us to explore what’s figuratively on our doorsteps. The Lovely Penelope (TLP) and I had a couple of short “staycations” (shoot me). I can thoroughly recommend the Tarr Farm Inn in the heart of the Exmoor National Park. A beautiful location and lovely place to stay: the oversized bathroom actually had a bath which, apparently, is important.

And now the summer hols are over, and the urchins are back where they belong: at school, being taught God-knows-what (it will probably involve a lot of Mary Seacole and/or that the entire world will be on fire by 2024). The road traffic is correspondingly heavier now than it has been at any time since this whole thing started back in January of last year. And I’ve never been happier to sit in it.

Why?

Clichéd image representing the season

Because we seem to be getting back to the good old days. Of working, of socialising, of fraternising. In essence: of living. There’s little point to being alive if you’re not actually “living”. Sleepy Uncle Joe (“the Afghanistan withdrawal was a complete success”) Biden is a testament to that, sadly.

No doubt the panjandrums in Whitehall are already looking for reasons to put us back into some sort of lockdown horror as soon as the totally normal Autumn-Winter cold season strikes (“Little Johnny in Year Three has just coughed: EVACUATE THE SCHOOL”).

Until then, enjoy the old normal. Take the time to appreciate those you love and whom you hold dear. And if you can do that in a restaurant or pub with a glass or two of something fermented, all the better: go and support our hospitality trade. God knows they need it.

“Never ask a barber if you need a haircut.”

FOUR: INDEX INVESTING TURNS 50!

HAPPY 50th TO THE WAY THAT CHANGED THE INVESTMENT WORLD

In mid-2008 I had some form of epiphany. Having been an Independent Financial Adviser (IFA) since May 2001 I finally had the nous to work out what I could control and what I could not. Firstly, I could - if I devoted myself to it - build a practice offering full-fat financial planning, with a relentless focus on helping people achieve their financial - and thus life - goals.

Secondly, with my coaching, I could help my clients/friends to control their reactions to external events and not bail out of their financial plans during times of stress. The most obvious example being our hard-wired proclivity to cash out of investments every time the markets experience a bog-standard temporary decline of 30% or more (happens on average every five to seven years).

Crucially, I would have full control over these two inputs of financial planning and behavioural coaching. With this came the acceptance that things I couldn’t control - the markets, the economy - should not concern me. From this, it was a natural progression to realising that picking “winning” fund managers and “timing the markets” was a fool’s errand.

What am I saying? I’m saying that since late 2008 I have used so-called index investing as the overarching theme behind the construction of client investment portfolios. The financial plan is the classy vehicle that will get my clients to their financial nirvana: the investment portfolio is just the fuel that drives said plan. Although vital, the fuel is not the focus. You don’t buy the beautiful car and then spend all your waking hours gazing adoringly at petrol pumps.

““Risk is measured as the probability that you won’t meet your financial goals. Investing should have the exclusive objective of minimising this risk.””

Thus an investment portfolio is just a means to an end. No plan = no portfolio, no exceptions, ever.

As a consequence, portfolio construction at Values to Vision FP Ltd goes something like this:

Me: “OK, we agree, Mr and Mrs Petrified, that you need to have accrued £X (we call this FU Money) if you want to have the choice to walk away from paid employment at age Y. Based on various assumptions - none of which will be borne out in reality - this looks achievable, as long as you salt away £Z amount every month from now until you hit age Y.

To reach your FU Money Pot target you need a return on those monthly savings of around 3-4% per annum over and above inflation. I don’t know of any other route that gives you the chance of doing this other than having a low-cost beautifully diversified portfolio chock full of the Great Companies Of The World.

Does that make sense? OK. Oh, and here’s an asinine risk questionnaire that my compliance people want you to suffer through. I like you both: let me fill it out for you, to save some time….”

You will note that in this diatribe not once do I mention which fund management group we are going to use to implement the investment portfolio. It’s just not important. We use funds that broadly track global markets, with a tilt to small-cap and value stocks. Dull, eh?

In essence, this is index - or passive - investing. And on 28th July it celebrated its 50th birthday. On 28th July 1971, Wells Fargo launched the first equity index fund with US$6 million from the Samsonite Corp pension fund.

It was an incredibly brave thing to do. Some called it - and still do - “un-American”. The notion that just matching the broad market rather than trying to “beat it” was a manly pursuit had many thinking Wall Street had lost its mind.

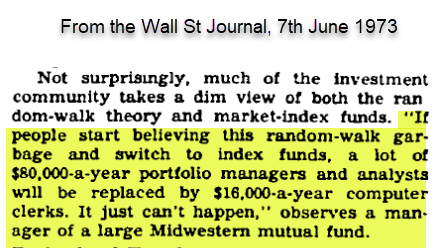

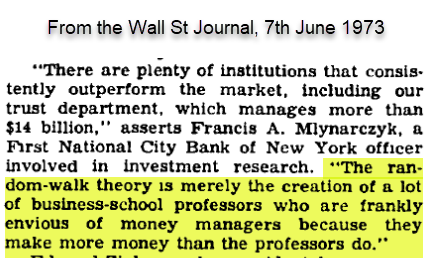

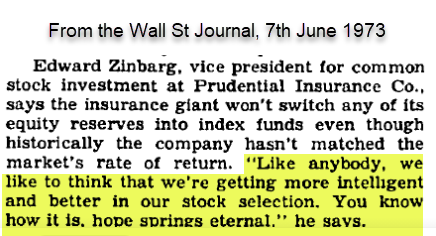

Indeed, the street’s journal managed to ignore the launch of the first index fund. It wasn’t until nearly two years later that the Wall Street Journal devoted serious coverage to this new fangled way of investing.

Take a look at the quotes above from its 7th June 1973 issue. Being kind: they have not aged well. Not at all. Today, the two largest asset management groups in the world - Blackrock and Vanguard - have built their businesses on index investing. I need not say more.

for the last 50 years, index investing has changed things for the better. this is a birthday to truly celebrate!

“I’ve lived through some terrible things in my life, some of which have happened.”

INFLATION IS TO RETIREMENT WHAT CARBON MONOXIDE IS TO HEALTH

This is a recurring piece. Each quarter the figures will be appropriately updated. Why? because while the numbers will change around the edges, the message is eternal!

A typical retired couple may well see one partner live for three decades or more. Over such a long period, the annual cost of Lifestyle could more than triple. Says who? Says me: financial planning involves enormous ambiguity. If you want certainty, die now.

So an example Lifestyle cost of £50,000 per annum entering retirement could later escalate to £150,000 a year, just to keep standing still, to keep buying the exact same amount of “stuff”.

If you really must, some prosaic evidence: in 1991 a First Class stamp cost 24p. Today? 85p. See detailed graph below:

Some nuggets to lessen the gloom (past performance is no guarantee of future returns etc):

Three decades ago - Autumn1991- the S&P 500 (The Great Companies of The USA) was valued at 387;

Today, 30 years on - Autumn 2021- The Great Companies of The USA are valued at c.4,500;

In three decades these Great Companies have grown in value by a factor of 12;

In addition, the dividends paid by these Great Companies have risen five-fold in those 30 years.

The last three decades have seen three severe "get me out of here I can't stand it anymore" bear markets (2001-3, 2007-9 and Q1 2020) and numerous smaller temporary declines.

Source for US market figures here. Why US data and not the UK? Because the Yanks have this kind of thing publicly available and we don't - yet. Also, the US market is enormous. By comparison, the UK market - at under 5% of worldwide market capitalisation - is tiny.

Dear Reader, the big risk to a dignified, independent retirement Lifestyle is the destruction of purchasing power via inflation. Like carbon monoxide, you can't hear it, smell it, see it, taste it. Yet inflation will silently, stealthily kill your wealth.

The cure? Possessing a Financial Plan fueled by ownership of The Great Companies of The World: equities.

The problem with the cure? It's really really hard to stick with your Plan and stay invested through the horrendous-but-always-temporary-declines. The cure for the cure? Having a tough-loving, empathetic counsellor to stand between you and "the big mistake".

Having stated the problem, and maybe scared you witless, I hope the above figures give you a glimpse as to the only rational, moral solution for a healthy couple facing a three-decade plus retirement!

“Inflation: odourless, tasteless, and utterly poisonous to a dignified, independent retirement.”